PAPER INDUSTRY WEEKLY REPORT (30/03/2026 – 03/04/2026)

Weekly paper industry report (30/03/2026 - 03/04/2026) compiled by Miza Joint Stock Company

Refer to the full weekly report at:

https://drive.google.com/file/d/1w7KK3jckIC4hVSdQjB88kc-0aTAIy_8Z/view?usp=sharing

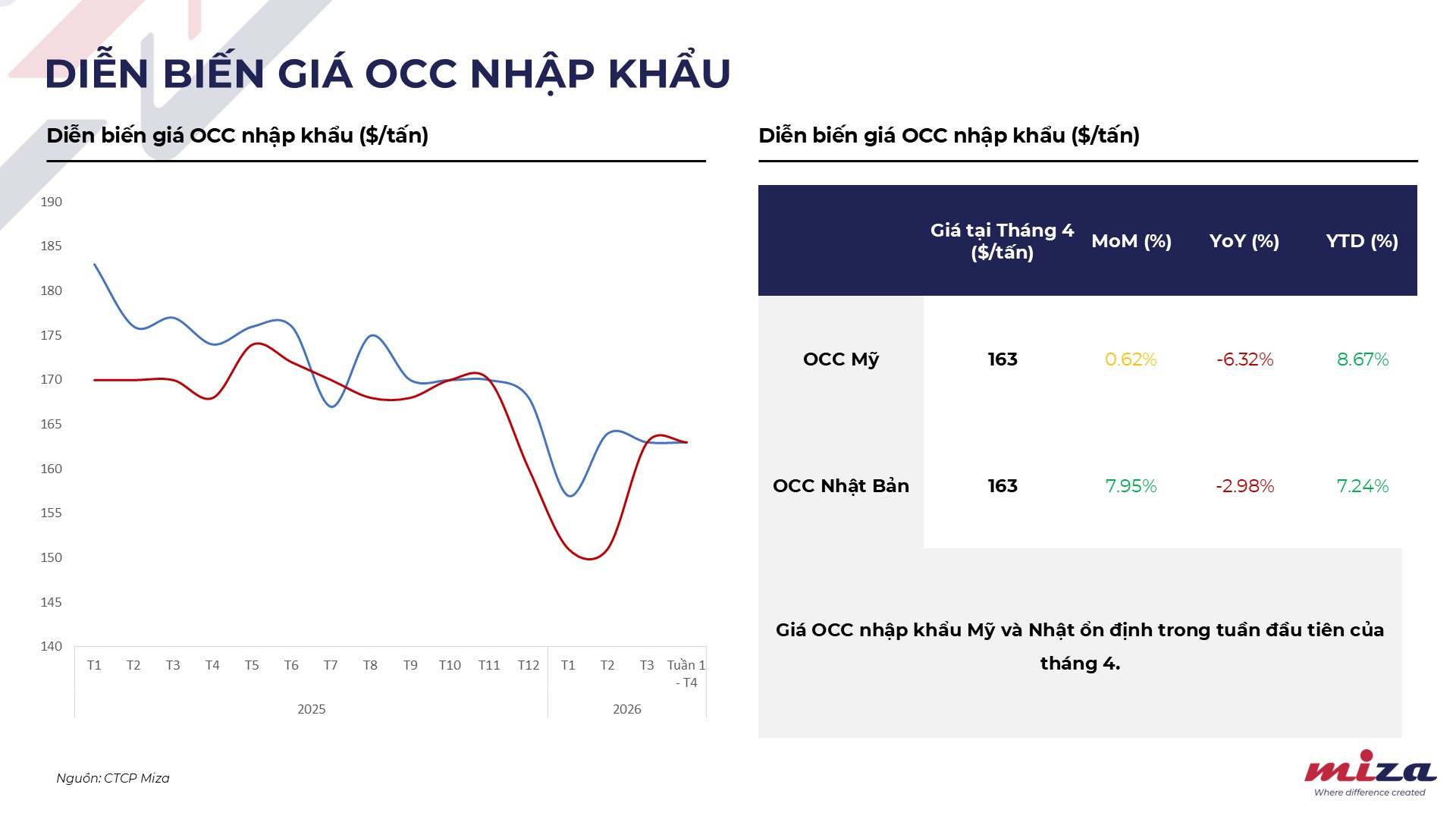

1. Price movements of imported OCC raw materials

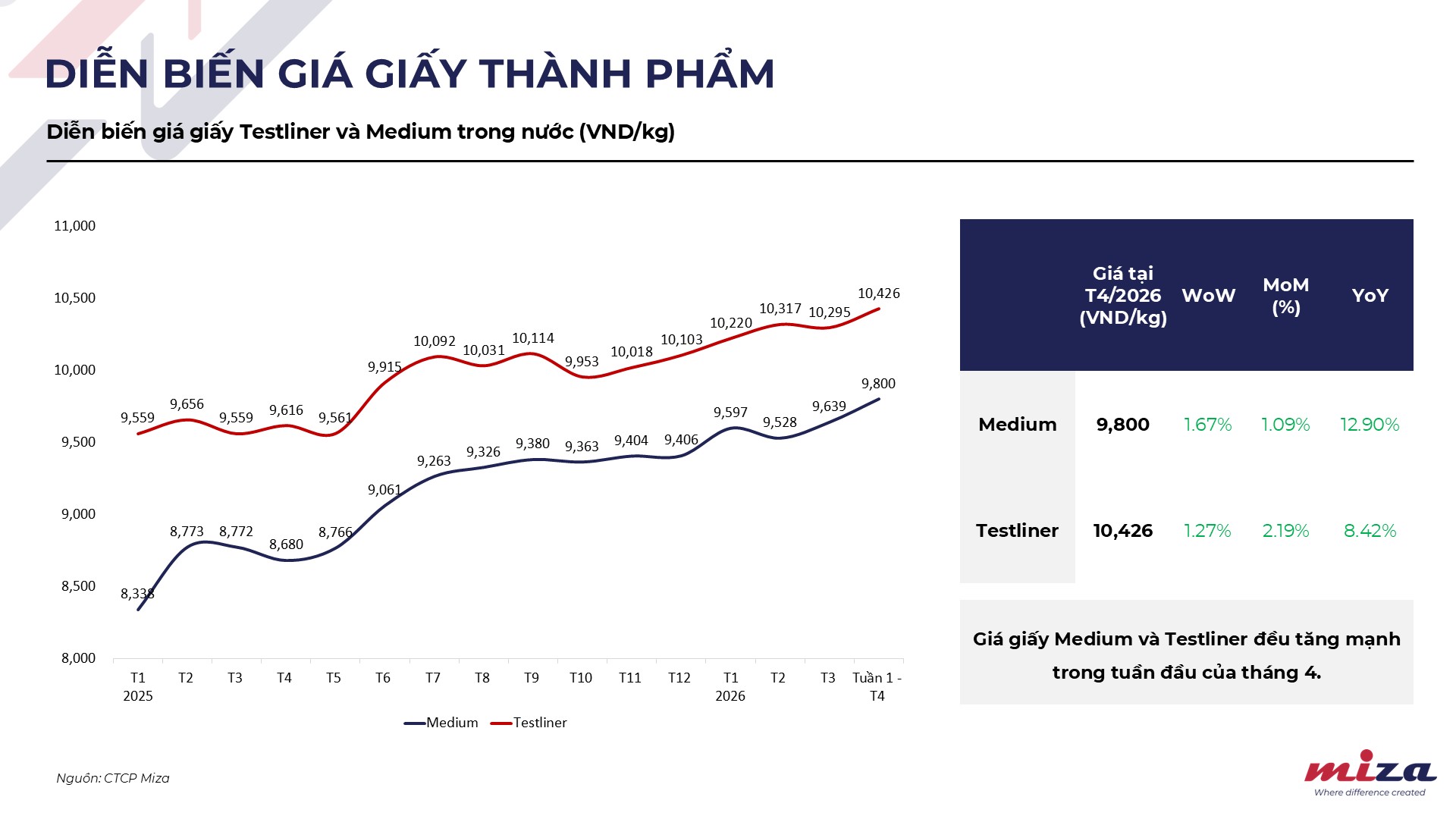

2. Movements in domestic finished paper prices

3. Highlights of the week

China's paper market reversed in early April 2026: Prices fell broadly due to weak demand: In early April 2026, China's paper market reversed rapidly when the previous rally ended and prices fell across the board. The main reason comes from weak demand in the low season, causing orders in the packaging and printing industry to not improve, making the previous price increase lacking a foundation and impossible to maintain. Large enterprises such as Nine Dragons Paper, Shanying Paper and Lee & Man Paper have simultaneously reduced the selling and purchase prices of scrap paper, pulling the market from seller to buyer status. Notably, Nine Dragons Paper also applies a discount of 50–100 yuan/ton with a short-term "price guarantee" policy, reflecting cautious sentiment and uncertainty about short-term price trends.

Indonesia tightens forest exploitation, causing the supply of hardwood pulp to drop sharply, putting pressure on the Asian market: Indonesia's tightening of forest exploitation has caused ~1 million hectares to be restricted, sharply reducing the supply of raw materials (~4 million tons of BHK/year), putting pressure on the Asian market. Businesses such as APRIL Group were directly affected (reduced production, increased imports), while Bracell switched to soluble powder, further narrowing the supply of BHK. As a result, the market turned to shortage concerns and accepted higher prices, mainly in hardwood pulp.

Featured Articles

TRADE UNION MEAL – CONNECTING LOVE, SPREADING HUMAN VALUES AT MIZA

28/7/2026

MIZA IS SINCERELY GRATEFUL – FOREVER GRATEFUL TO THE HEROES AND MARTYRS

27/7/2026

NHK WORLD-JAPAN RECORDED AND INTERVIEWED THE CHAIRMAN OF THE BOARD OF DIRECTORS OF MIZA GROUP AFTER THE MZG LISTING MILESTONE ON HOSE

17/7/2026

MIZA LISTS HOSE: AMBITION TO LEAD THE PAPER INDUSTRY

1/7/2026

MIZA GROUP ACCOMPANIES THE IX "BEYOND FATE" CONTEST

23/5/2026